The Financial Sector (Climate-related Disclosures and Other Matters) Amendment Act 2021 (Climate-related Disclosures Act) was enacted on 27 October 2021. The Climate-related Disclosures Act introduces several new obligations on climate-reporting entities (CREs), including the obligation to prepare climate statements under subpart 3 of Part 7A of the Financial Markets Conduct Act 2013 (FMCA), as amended by the Climate-related Disclosures Act.1

CREs will be under an obligation to prepare climate statements under section 461Z of the FMCA, unless they fall under an exemption under subsection (2). Where CREs have one or more subsidiaries, the obligation is to prepare group climate statements under section 461ZA of the FMCA (as opposed to climate statements on an individual basis).

This article outlines the information that the External Reporting Board (XRB), the New Zealand crown entity responsible for developing and issuing the climate related disclosure framework, has proposed to be included in climate statements or group climate statements (as the case may be) and considers whether New Zealand CREs with one or more subsidiaries will require support from their subsidiaries in order to meet their obligation to prepare group climate statements.

Information to be contained in climate statements

The information that will need to be included in climate statements or group climate statements will be determined by the XRB.

In October last year, the XRB published its first consultation document on Aotearoa New Zealand Climate Standard 1: Climate-related Disclosures (NZ CS 1) and sought feedback on the draft governance and risk management sections. In March, the XRB published its second consultation document and consulted on the draft strategy, and metrics and targets sections of NZ CS 1.

From the two NZ CS 1 consultation documents, the XRB proposes CREs to disclose the following information in their climate statements and group climate statements:2

| Sections of NZ CS 1 | Disclosure objective | Proposed disclosures under this section |

| Governance | To enable primary users to understand both the role an entity’s board plays in overseeing climate-related issues, and the role management plays in assessing and managing those issues. Such information supports evaluations by primary users of whether climate-related issues receive appropriate board and management attention. |

An entity must disclose the following information:

|

| Risk management | To understand how an entity’s climate-related risks are identified, assessed and managed, and how those processes are integrated in existing risk management processes. Together with the Strategy disclosures, such information supports evaluations by primary users of the entity’s overall risk profile and the quality and robustness of the entity’s risk management activities. |

An entity must disclose the following information for both transition risks (being, the risks relating to the transition to a lower-emissions global and domestic economy) and physical risks:

|

| Strategy | To understand the impacts of climate-related risks and opportunities on an entity’s business model, strategy and financial planning over the short, medium, and long term, including actual and potential financial impacts. How an entity has employed scenario analysis to evaluate the resilience of its business model and strategy is a key factor in realising this objective. Such information is used to inform expectations about the future performance of an entity. |

An entity must disclose:

|

| Metrics and targets | To enable primary users to understand how an entity measures and manages its climate-related risks and opportunities. Such information supports primary user’s evaluations of the entity’s potential risk-adjusted returns, ability to meet financial obligations, general exposure to climate-related risks and opportunities, and progress in managing or adapting to those risks and opportunities. They also provide a basis upon which primary users can compare entities within a sector or industry. |

An entity must disclose:

|

Commencement of the new reporting regime

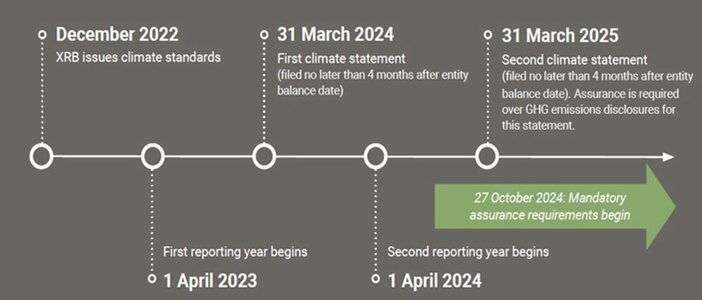

The mandatory reporting regime under the Climate-related Disclosures Act takes effect for accounting periods that start on or after the XRB issues the final version of the first climate standard. The XRB has indicated that it will release a formal exposure draft of NZ CS 1 and other supporting standards for consultation in July 2022, with the intention to issue the final climate standards by December 2022 (together known as the climate-related disclosure framework).3

This means that CREs with a 31 March balance date must ensure that they are in position to file their first group climate statements for the first reporting year (ie 1 April 2023 to 31 March 2024) by 31 July 2024 (ie climate statements must be filed no later than four months after the balance date). The XRB's example timeline for an entity with a 31 March balance date is set out below (see also page 12 of the Strategy, and Metrics and Targets Consultation Document dated March 2022):

Uncertainty in relation to the support required from subsidiaries

Most CREs will now be considering the policies and processes that they will need to implement to ensure that they will be able to prepare climate statements or group climate statements, as the case may be, once this new regime commences.

In the case of CREs preparing group climate statements, we have noticed that the consultation documents are silent on the information that these CREs will need to disclose for their subsidiaries, the level of detail that needs to be disclosed, and how this information should be presented. The XRB has heard the concerns around how group climate reporting can occur, with one submission also asking the question whether "parent companies are required to disclose the risk management and governance processes for their subsidiaries?".4

We anticipate that the parent companies will be required to disclose certain information relating to their subsidiaries to ensure that their group climate statements are meaningful when disclosed to primary users (being existing and potential investors, lenders, and other creditors).

Accordingly, the parent companies will need the support from their subsidiaries in preparing their group climate statements. However, the level of support that is required from the subsidiaries is currently unclear given that the consultation papers do not expressly address the information that parent companies need to disclose for their subsidiaries. We expect that the XRB will clarify this once the exposure draft of NZ CS 1 and the accompanying guidance are released in July.

In the meantime, CREs may wish to start having preliminary discussions with their subsidiaries in relation to the obligation to prepare group climate statements and the impact this obligation may have on both parent and subsidiary. While certain subsidiaries will be more well equipped to support their parent company if required (eg where the subsidiary is itself a CRE), there could be some growing pains for other subsidiaries if the parent company requests support, especially in the circumstances where that subsidiary itself is not a CRE and operates its business independently from the parent company.

Accordingly, we think it would be an opportune time for both parent and subsidiary to have these preliminary discussions now (as opposed to waiting until the XRB issues the final version of NZ CS 1 in December 2022) to ensure that subsidiaries capture the relevant information that must be provided to their parent company in time to meet the first reporting deadline.

Financial Market Authority's implementation approach

The Financial Market Authority (FMA) published its implementation approach to the climate reporting regime in November last year.5 In the early stages of the regime, the FMA envisages taking a broadly educative and constructive approach (as opposed to a monitoring and enforcement approach), with a focus on issuing high level guidance on compliance expectations. However, the FMA has indicated that it will take enforcement action if there is serious misconduct, which includes the failure to produce climate statements or where climate statements are misleading or false.

Closing comments

If you would like advice on how the Climate-related Disclosures Act may impact you, please contact a member of our financial services regulation team.

1 This article references the provisions of the FMCA, as amended by the Climate-related Disclosures Act.

2 See Governance and Risk Management Consultation Document dated October 2021 and Strategy, and Metrics and Targets Consultation Document dated March 2022.

3 For completeness, we note that the XRB has stated it will also be releasing a formal exposure draft of Aotearoa New Zealand Climate Standard 2: First-time Adoption of Aotearoa New Zealand Climate Standard (NZ CS 2) and Aotearoa New Zealand Climate Standard 3: General requirements for Climate-related Disclosures (NZ CS 3) in July 2022. We have not considered or discussed NZ CS 2 or NZ CS 3 in this article.

4 See page 10 of XRB's "What we heard" document dated February 2022, which summarises the feedback the XRB received in respect of the Governance and Risk Management sections of NZ CS 1 Consultation Paper.

5 A copy of the FMA's implementation approach to the Climate-related Disclosures regime can be found here.